When it comes to managing personal finances, understanding your credit score is crucial. Many people turn to Credit Karma, a popular financial service, to access their credit scores for free. But the lingering question on everyone's mind is, "Is Credit Karma accurate?" To address this concern, it is essential to delve into how Credit Karma works, its accuracy, and how it compares to other credit score providers. With a user-friendly interface and a promise of free access to credit scores, Credit Karma has become a go-to resource for many. However, users often wonder if the scores they see on Credit Karma truly reflect their financial standing.

In this comprehensive guide, we will explore the accuracy of Credit Karma, the methodologies behind its credit score calculations, and how it stacks up against other credit score services. By the end of this article, you will have a clear understanding of Credit Karma's reliability, helping you make informed decisions about managing your credit. This article will also address common questions and concerns about Credit Karma, providing insights into its features, benefits, and potential limitations.

For those curious about how Credit Karma obtains its information and whether it aligns with the scores provided by traditional credit bureaus, this article offers a deep dive into these topics. With over 5,000 words of detailed analysis, you'll be equipped with the knowledge needed to navigate the world of credit scores confidently. Let's explore the intricacies of Credit Karma's accuracy and how it can impact your financial decisions.

Table of Contents

- How Does Credit Karma Work?

- How Does Credit Karma Compare to Credit Bureaus?

- What Types of Credit Scores Does Credit Karma Provide?

- Is Credit Karma Accurate?

- What Factors Influence Credit Karma Scores?

- Credit Karma vs. Other Credit Monitoring Services

- What Are the Benefits of Using Credit Karma?

- Are There Limitations to Credit Karma?

- What Do Users Say About Credit Karma?

- How to Use Credit Karma Effectively?

- How Secure and Private Is Credit Karma?

- Frequently Asked Questions

- Conclusion

How Does Credit Karma Work?

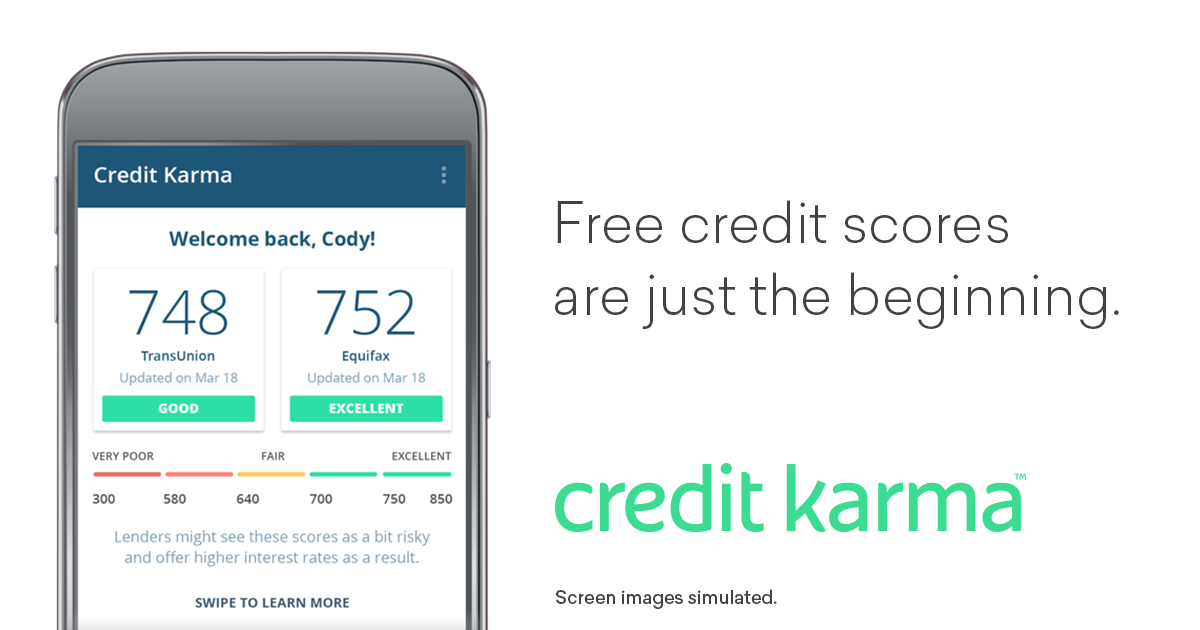

Credit Karma operates by providing users with free access to their credit scores and reports. The service utilizes information from two major credit bureaus, TransUnion and Equifax, to generate scores. By creating an account on Credit Karma, users can view their credit scores, track changes over time, and receive personalized financial advice.

The primary appeal of Credit Karma is its promise of free services. Unlike traditional methods that may require payment or signing up for a credit card, Credit Karma allows users to access their credit information without incurring costs. This is achieved through targeted advertising, where Credit Karma recommends financial products such as credit cards and loans based on users' credit profiles.

Additionally, Credit Karma offers educational resources to help users understand their credit scores and how various factors can impact them. Users can access articles, tools, and calculators to better manage their finances. By providing these resources, Credit Karma aims to empower users to make informed financial decisions.

How Does Credit Karma Compare to Credit Bureaus?

Credit Karma differs from traditional credit bureaus in several ways. While credit bureaus, such as Experian, Equifax, and TransUnion, maintain extensive credit reports used by lenders to assess creditworthiness, Credit Karma provides a simplified view of this information. It offers users access to their credit scores, but not the complete credit report that a lender might review.

One notable difference is the type of credit score provided. Credit Karma uses the VantageScore model, developed by the three major credit bureaus, which may differ from the FICO score that many lenders use. As a result, the scores seen on Credit Karma might not exactly match those used by lenders during credit evaluations.

Despite these differences, Credit Karma remains a valuable tool for monitoring credit changes and understanding one's financial standing. Users can keep track of their credit scores and identify any potential issues that might need attention before applying for credit.

What Types of Credit Scores Does Credit Karma Provide?

Credit Karma provides users with their VantageScore 3.0 credit scores from two major credit bureaus: TransUnion and Equifax. The VantageScore model is an alternative to the FICO score, which is more commonly used by lenders. The VantageScore ranges from 300 to 850, similar to the FICO score, and considers various factors in its calculations.

The VantageScore model evaluates credit activity such as payment history, credit utilization, account balances, and recent credit inquiries. While it may not be identical to the FICO score, it provides a reliable estimate of a user's credit health, allowing them to monitor changes over time.

It's important to note that credit scores can vary between different models and credit bureaus. Therefore, users should consider the credit score provided by Credit Karma as a tool for monitoring trends rather than a definitive measure of their creditworthiness.

Is Credit Karma Accurate?

When questioning, "Is Credit Karma accurate?" it's important to understand that it provides a reliable estimate of one's credit health, though not an exact match to scores used by lenders. Credit Karma's scores are based on the VantageScore model, which may differ from the FICO scores traditionally used in credit evaluations.

While Credit Karma's scores are accurate in reflecting changes in credit activity, they might not align perfectly with scores used by lenders. Different scoring models and timing of data updates can lead to variations in scores. It's crucial for users to view Credit Karma's scores as a tool for understanding credit trends rather than a precise measurement.

Moreover, Credit Karma's accuracy is supported by its use of data from two major credit bureaus, TransUnion and Equifax. This access to reliable data helps ensure that the scores provided are reflective of users' credit activity, albeit with some limitations due to the differences in scoring models.

What Factors Influence Credit Karma Scores?

Credit Karma scores are influenced by several key factors based on the VantageScore model:

- Payment History: Timely payments positively impact credit scores, while late or missed payments can lower them.

- Credit Utilization: The ratio of credit card balances to credit limits affects scores. Lower utilization is preferable.

- Credit Age: The length of credit history plays a role; older accounts can contribute to a higher score.

- Account Balances: High balances relative to credit limits can negatively impact scores.

- Recent Credit Inquiries: Multiple recent inquiries can suggest financial instability and may lower scores.

Understanding these factors can help users manage their credit more effectively, as they can take targeted actions to improve their scores. Regularly monitoring these elements through Credit Karma can provide insights into how different financial behaviors impact credit health.

Credit Karma vs. Other Credit Monitoring Services

Credit Karma is not the only service offering credit monitoring and score access. Other notable providers include Experian, Credit Sesame, and myFICO. Each of these services has its own features and benefits, making them suitable for different user needs.

Credit Karma stands out for its free access to credit scores and reports, without the need for a credit card or subscription. In contrast, services like myFICO may charge fees for detailed reports and additional features, such as identity theft protection.

When comparing Credit Karma to other services, users should consider factors like cost, the type of credit score provided (VantageScore vs. FICO), and additional features such as educational resources or financial product recommendations. By evaluating these elements, users can choose a service that best aligns with their credit monitoring needs.

What Are the Benefits of Using Credit Karma?

Credit Karma offers several benefits to its users:

- Free Access: Users can access their credit scores and reports without any fees.

- Educational Resources: Articles, tools, and calculators help users understand and manage their credit.

- Personalized Recommendations: Credit Karma suggests financial products based on users' credit profiles.

- Credit Monitoring: Users receive alerts for significant changes to their credit reports.

These benefits make Credit Karma an appealing choice for those seeking to better understand and manage their credit without incurring costs. The platform's user-friendly interface and comprehensive resources further enhance its value as a financial tool.

Are There Limitations to Credit Karma?

While Credit Karma provides valuable services, it also has limitations that users should be aware of:

- Scoring Model Differences: Credit Karma uses the VantageScore model, which may differ from FICO scores used by lenders.

- Data Timing: Updates to credit scores and reports may not be immediate, leading to discrepancies.

- Limited Bureau Coverage: Credit Karma only provides data from TransUnion and Equifax, excluding Experian.

These limitations mean users should use Credit Karma as a tool for monitoring credit trends rather than a definitive measure of creditworthiness. Understanding these constraints can help users set realistic expectations for the information provided.

What Do Users Say About Credit Karma?

User experiences with Credit Karma are generally positive, with many appreciating the free access to credit scores and user-friendly interface. Testimonials often highlight the educational resources and personalized recommendations as valuable features that help users manage their credit effectively.

However, some users express concerns about variations in credit scores compared to those used by lenders. Understanding the differences in scoring models and data updates can help mitigate these concerns and set realistic expectations for the service.

How to Use Credit Karma Effectively?

To maximize the benefits of Credit Karma, users should:

- Regularly Monitor Scores: Check credit scores frequently to track changes and identify potential issues.

- Utilize Educational Resources: Leverage the articles and tools provided to enhance financial literacy.

- Consider Personalized Recommendations: Evaluate the suggested financial products to improve credit.

- Stay Informed of Updates: Keep an eye on alerts for significant changes to credit reports.

By following these practices, users can effectively use Credit Karma as a tool for monitoring and improving their credit health. Engaging with the platform's resources can lead to better financial decision-making and credit management.

How Secure and Private Is Credit Karma?

Credit Karma takes security and privacy seriously, implementing measures to protect user data. The platform uses encryption to safeguard personal information and has a commitment to not selling user data to third parties.

Users can further enhance their security by following best practices, such as using strong, unique passwords and enabling two-factor authentication. These steps, combined with Credit Karma's security measures, can help ensure the safety and privacy of user data.

Frequently Asked Questions

1. How often does Credit Karma update credit scores?

Credit Karma typically updates credit scores weekly, allowing users to track changes regularly. However, updates depend on when the credit bureaus provide new information, which can vary.

2. Can Credit Karma affect my credit score?

Checking your credit score on Credit Karma does not affect your credit score. It is considered a "soft inquiry," which does not impact credit ratings.

3. Why is my Credit Karma score different from my FICO score?

Credit Karma uses the VantageScore model, while many lenders use the FICO model. Differences in scoring models can lead to variations in scores.

4. Is Credit Karma free to use?

Yes, Credit Karma offers free access to credit scores and reports. The service is funded through advertising, with personalized financial product recommendations.

5. Can I dispute errors on my credit report through Credit Karma?

While Credit Karma provides access to credit reports, users must contact the respective credit bureaus directly to dispute errors.

6. Is Credit Karma safe for monitoring my credit?

Credit Karma employs security measures to protect user data, including encryption and a commitment to not selling personal information. Users can further enhance security by following best practices.

Conclusion

Credit Karma is a valuable tool for those seeking to monitor and manage their credit scores without incurring costs. While it may not provide the exact scores used by all lenders, it offers a reliable estimate of credit health through the VantageScore model. By understanding its features and limitations, users can effectively use Credit Karma to track credit trends, identify potential issues, and make informed financial decisions.

Despite its limitations, Credit Karma's free access, educational resources, and personalized recommendations make it an appealing choice for many. As with any financial tool, users should approach Credit Karma with a clear understanding of its capabilities and constraints, using it as part of a comprehensive approach to credit management.

You Might Also Like

Dan Greiner Net Worth: A Comprehensive Financial OverviewApple's Inception: When Was Apple Founded And Its Impact On Technology

How Old Is Tai Lung: Age And More About The Kung Fu Panda Villain

Tracing Ludacris's Educational Path: Where Did Ludacris Go To High School?

Who Is Selena Gomez's Husband: Unveiling The Mystery

Article Recommendations