Credit Karma provides its users with credit scores and reports derived from two of the three major credit bureaus in the United States. While this might sound reassuring, differences in scoring models and data reporting can lead to variations in the score you see on Credit Karma versus what a lender might see. This discrepancy often leads to confusion, prompting users to question the accuracy of the scores provided. In this comprehensive article, we'll delve into the intricacies of Credit Karma's accuracy, examine how it compares to other credit scoring systems, and provide insights into making the best use of this financial tool. We'll also explore frequently asked questions, addressing common concerns and misconceptions to provide a clearer understanding of what to expect from Credit Karma. By the end of this article, you'll have a solid grasp of how reliable Credit Karma is and how to effectively use it as a part of your financial health strategy.

Table of Contents

1. What is Credit Karma? 2. How Does Credit Karma Work? 3. Credit Karma vs. FICO: What's the Difference? 4. Why Do Credit Scores Vary? 5. How Accurate is Credit Karma? 6. Benefits of Using Credit Karma 7. Limitations of Credit Karma 8. How to Use Credit Karma Effectively 9. Are There Alternatives to Credit Karma? 10. Credit Karma and Your Financial Health 11. User Experiences with Credit Karma 12. Is Credit Karma Secure? 13. Common Misconceptions About Credit Karma 14. FAQs About Credit Karma 15. Conclusion

What is Credit Karma?

Credit Karma is a financial technology company best known for providing free credit scores and reports to consumers. Founded in 2007 by Kenneth Lin, Credit Karma has grown rapidly, offering a range of financial services beyond just credit monitoring. With millions of users, it serves as a valuable tool for individuals looking to improve their financial literacy and management.

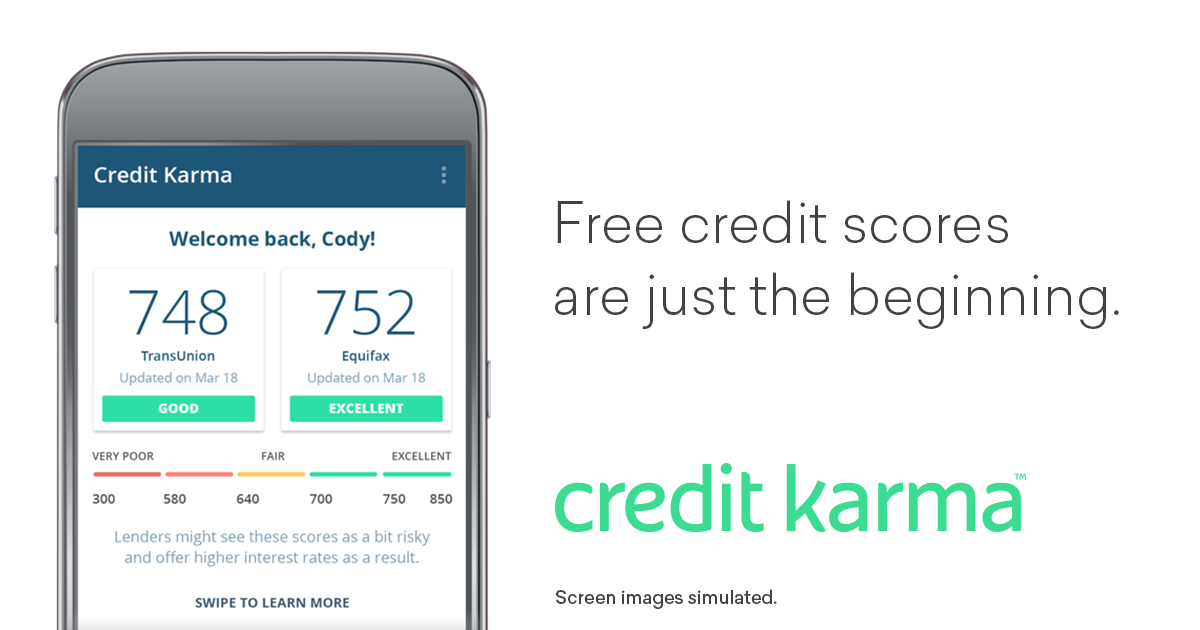

Credit Karma sources its credit scores from two of the three major credit bureaus in the United States—TransUnion and Equifax. This is important because each bureau may have different information about a consumer's credit history, leading to variations in credit scores. Credit Karma uses the VantageScore 3.0 model, which differs from the FICO scores that many lenders use.

Beyond credit scores, Credit Karma also provides users with personalized financial recommendations, insights into their credit reports, and tools to help them manage their finances. The platform generates revenue by suggesting financial products, such as credit cards and loans, that users may be eligible for based on their credit profiles.

How Does Credit Karma Work?

Credit Karma operates by leveraging data from TransUnion and Equifax to provide users with a snapshot of their credit health. Users create a free account, which gives them access to their credit scores, credit reports, and a suite of financial tools. Credit Karma updates these scores weekly, allowing users to track their credit progress over time.

The platform employs the VantageScore 3.0 model to calculate credit scores. This model considers factors such as payment history, credit utilization, and the age of credit accounts. It's worth noting that while VantageScore is widely used, it may differ from the FICO score, which is the standard for most lenders.

Credit Karma also offers personalized recommendations for financial products, including credit cards and loans. These recommendations are based on the user's credit profile, helping them make informed choices about which products are likely to be a good fit. The company earns money through referral fees when users apply for these products through their platform.

Credit Karma vs. FICO: What's the Difference?

One of the most common sources of confusion for Credit Karma users is the difference between the scores they see on the platform and their FICO scores. FICO scores are the most widely used credit scores by lenders, developed by the Fair Isaac Corporation. In contrast, Credit Karma uses the VantageScore 3.0 model from TransUnion and Equifax.

The key differences between FICO and VantageScore include:

- Scoring Models: FICO and VantageScore use different algorithms to calculate credit scores, considering slightly different factors and weights.

- Score Range: Both FICO and VantageScore have a range of 300 to 850, but the scores can still differ significantly due to the distinct models used.

- Data Sources: Credit Karma pulls data from two credit bureaus, while FICO scores can be based on data from one, two, or all three major credit bureaus.

As a result, users may notice discrepancies between their Credit Karma scores and the FICO scores lenders use. This does not necessarily mean one is inaccurate; rather, they are simply calculated using different criteria.

Why Do Credit Scores Vary?

Credit scores can vary due to differences in the data used, the scoring model applied, and the timing of updates. Each credit bureau collects data independently, which means they may have different information about a consumer's credit history. This can lead to variations in the scores provided by each bureau.

Additionally, different scoring models, such as FICO and VantageScore, have distinct algorithms that weigh factors differently. This can result in different scores even if the underlying data is the same. Furthermore, the frequency of updates can affect scores. Credit Karma updates weekly, while some lenders may use older data, leading to discrepancies.

Understanding these nuances is key to interpreting credit scores accurately. It's important to monitor scores across different platforms and models to get a comprehensive view of one's credit health.

How Accurate is Credit Karma?

The accuracy of Credit Karma largely depends on what users expect from the platform. Credit Karma provides a reliable approximation of a user's credit health, using data from two major credit bureaus and the VantageScore 3.0 model. However, it's crucial to remember that lenders may use different models, such as FICO, which can result in varying scores.

While Credit Karma is a valuable tool for monitoring credit trends and understanding credit factors, it may not precisely match the scores used by lenders. This doesn't imply inaccuracy; rather, it highlights the differences in scoring models and data sources. For most users, Credit Karma offers an accurate reflection of their credit status, suitable for personal monitoring and improvement.

For those seeking the exact score a lender might use, obtaining a FICO score directly from a credit bureau or through a financial institution may be necessary. However, for regular monitoring and educational purposes, Credit Karma remains a highly effective resource.

Benefits of Using Credit Karma

Credit Karma offers numerous benefits that make it a popular choice among consumers looking to manage their credit health:

- Free Access: Users can access their credit scores and reports free of charge, without affecting their credit scores.

- Regular Updates: Credit Karma updates scores weekly, allowing users to track changes and progress over time.

- Educational Tools: The platform provides resources and insights to help users understand credit factors and improve their scores.

- Personalized Recommendations: Users receive tailored suggestions for credit products that match their profiles, potentially saving money and improving credit.

- Comprehensive Insights: Credit Karma offers a detailed breakdown of credit reports, highlighting areas for improvement.

These benefits make Credit Karma a valuable tool for anyone looking to maintain and improve their credit health.

Limitations of Credit Karma

Despite its advantages, Credit Karma has certain limitations that users should be aware of:

- Different Scoring Models: Credit Karma uses the VantageScore model, which may differ from the FICO scores used by many lenders.

- Limited Bureau Data: Credit Karma pulls data from only two of the three major credit bureaus, possibly missing information from Experian.

- Potential Discrepancies: Users may experience discrepancies between Credit Karma scores and those seen by lenders, leading to confusion.

- Product Recommendations: While personalized, recommended products may not always be the best fit for every user, making independent research necessary.

Understanding these limitations is crucial for effectively using Credit Karma alongside other credit monitoring tools and resources.

How to Use Credit Karma Effectively

To maximize the benefits of Credit Karma, users should follow these strategies:

- Regular Monitoring: Check credit scores and reports regularly to stay informed about any changes or potential issues.

- Understand the Factors: Familiarize yourself with the factors affecting credit scores, such as payment history and credit utilization, to make informed decisions.

- Use Recommendations Wisely: Evaluate recommended products carefully, considering other options and conducting independent research.

- Focus on Improvement: Utilize Credit Karma's insights to identify areas for improvement and take actionable steps to enhance your credit health.

By using these strategies, users can effectively leverage Credit Karma as part of their overall financial management plan.

Are There Alternatives to Credit Karma?

While Credit Karma is a popular choice for credit monitoring, several alternatives offer similar services:

- Experian: Provides free access to FICO scores, credit reports, and monitoring tools.

- Credit Sesame: Offers free credit scores, identity theft protection, and personalized financial advice.

- Mint: A comprehensive financial management tool that includes credit score monitoring.

- AnnualCreditReport.com: Allows users to access free credit reports from all three major bureaus once a year.

These alternatives provide different features and services, allowing users to choose the best option based on their needs and preferences.

Credit Karma and Your Financial Health

Credit Karma plays a significant role in helping users manage their financial health. By providing free access to credit scores and reports, it empowers individuals to take control of their credit and make informed financial decisions.

Understanding one's credit health is crucial for obtaining loans, credit cards, and favorable interest rates. Credit Karma's tools and insights help users identify areas for improvement, track progress, and work towards achieving their financial goals.

By using Credit Karma in conjunction with other financial resources, individuals can develop a comprehensive understanding of their financial situation and take proactive steps to enhance their overall financial health.

User Experiences with Credit Karma

Many users have shared positive experiences with Credit Karma, highlighting its ease of use, comprehensive insights, and helpful tools. Users appreciate the regular updates to their credit scores and the ability to track their credit progress over time.

However, some users have expressed concerns about discrepancies between Credit Karma scores and those seen by lenders, as well as the limited data from only two credit bureaus. Despite these concerns, the majority of users find Credit Karma to be a valuable resource for monitoring and improving their credit health.

Overall, user experiences indicate that Credit Karma is an effective tool for understanding and managing credit, provided users are aware of its limitations and use it alongside other resources.

Is Credit Karma Secure?

Security is a top priority for Credit Karma, and the platform employs robust measures to protect user data. This includes encryption, two-factor authentication, and regular security audits.

Users can take additional steps to secure their accounts, such as using strong, unique passwords and enabling two-factor authentication. By following these best practices, users can confidently use Credit Karma while safeguarding their personal information.

Overall, Credit Karma is considered a secure platform, making it a trusted choice for those looking to monitor their credit health and financial well-being.

Common Misconceptions About Credit Karma

Several misconceptions about Credit Karma may lead to confusion among users:

- Inaccuracy: Some believe Credit Karma scores are inaccurate, but they simply use a different scoring model (VantageScore) than lenders (FICO).

- Data Security: Concerns about data security are common, but Credit Karma employs strong security measures to protect user information.

- Limited Bureau Data: While Credit Karma uses data from two bureaus, users can access their Experian data through other platforms for a comprehensive view.

Understanding these misconceptions can help users make informed decisions about how to use Credit Karma effectively.

FAQs About Credit Karma

1. How often does Credit Karma update my credit score?

Credit Karma updates your credit score weekly, allowing you to track changes and progress over time.

2. Does using Credit Karma affect my credit score?

No, checking your credit score on Credit Karma is considered a soft inquiry and does not affect your credit score.

3. Why is my Credit Karma score different from my FICO score?

Credit Karma uses the VantageScore model, which may differ from the FICO model used by lenders, resulting in different scores.

4. Can Credit Karma help me improve my credit score?

Yes, Credit Karma provides insights and recommendations to help you identify areas for improvement and take steps to enhance your credit score.

5. Is Credit Karma really free?

Yes, Credit Karma offers free access to credit scores, reports, and financial tools without any hidden fees.

6. How secure is my information on Credit Karma?

Credit Karma employs robust security measures, including encryption and two-factor authentication, to protect user data.

Conclusion

In conclusion, Credit Karma is a valuable tool for monitoring and understanding your credit health. While it may not provide the exact scores used by lenders, it offers a reliable approximation for personal use. By understanding the differences between Credit Karma and other scoring models, such as FICO, users can make informed financial decisions and take steps to improve their credit health.

Despite its limitations, Credit Karma remains an effective resource for tracking credit progress and educating users about the factors affecting their scores. By using Credit Karma alongside other financial tools and resources, individuals can gain a comprehensive understanding of their financial situation and work towards achieving their financial goals.

For those seeking to better manage their credit and financial health, Credit Karma is a trusted and secure platform that provides valuable insights and recommendations, empowering users to take control of their financial future.

You Might Also Like

Discovering The Financial Journey Of Lorenzo Luaces: A Deep Dive Into His Net WorthSecrets To Selfish Romance: A Guide For Modern Love

The Rise Of Matt Rife: Early Years And Beyond

Stylish Beard No Mustache Styles: A Trendy Guide

Water Weight Matters: How Much Does 5 Gallons Of Water Weigh?

Article Recommendations

- East Multnomah Soil And Water Conservation District

- Natural Hairstyles Crossword

- Rufus Du Sol Los Angeles